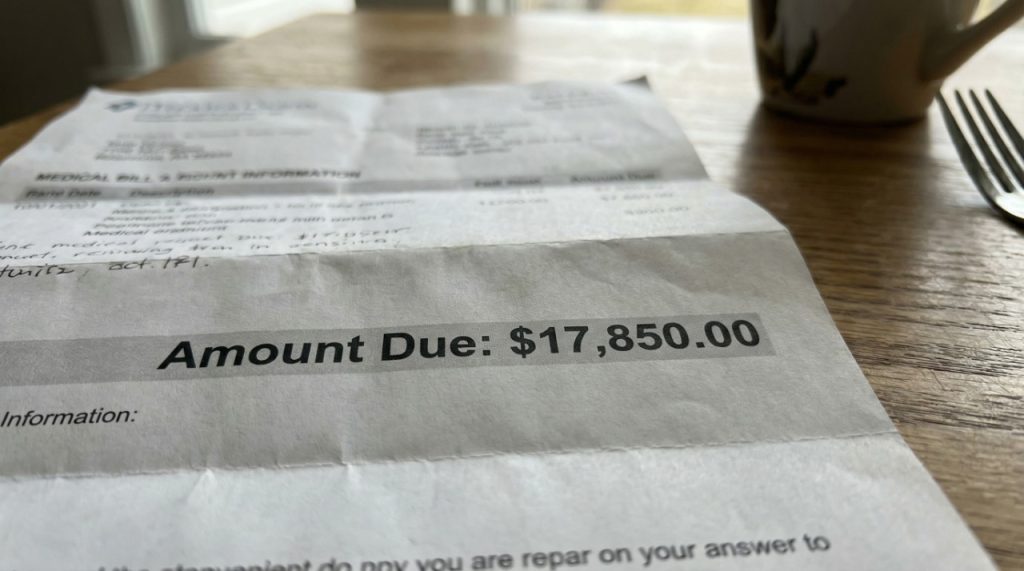

The bill was $17,850.

Her insurance covered almost nothing.

And it started with something that seemed entirely minor.

Elizabeth Moreno, a college student from Texas, needed a routine checkup before a minor back surgery. Her doctor asked for a standard urine test.

She went to an in-network clinic. She paid her regular copay. She walked out thinking everything was handled.

But a few weeks later, a letter arrived in the mail that completely derailed her financial life.

The invoice wasn’t from her doctor. It was from an out-of-state laboratory she had never even heard of.

The lab was charging an astronomical $17,850 to test one small urine sample. Her insurer, Blue Cross Blue Shield, paid just over $100, declaring the charges wildly excessive.

The laboratory expected Elizabeth to pay the remaining $17,750 out of her own pocket.

But that wasn’t the real problem.

The true nightmare was a dangerous insurance gap hidden in the fine print of American healthcare.

Even though Elizabeth carefully chose an in-network doctor, that doctor sent her sample to an out-of-network lab without her consent. Because the lab had no contract with her insurer, her standard liability coverage and out-of-pocket deductible limits didn’t protect her.

This is the “surprise billing” trap. Millions of Americans face this exact liability issue every year. Without aggressive legal settlement negotiations or specialized umbrella policies, a simple clinic visit can quickly force a family into bankruptcy.

Here is exactly how the billing trap works for a routine lab test:

- With standard in-network policy: $10 – $50

- Without coverage (self-pay): $150 – $300

- The “Out-of-Network” Surprise Trap: $17,850

Most Americans assume insurance covers this. It often doesn’t.

Before your next medical appointment, take these steps to protect your wallet and close your coverage gaps:

- Demand network verification: Always explicitly ask, “Are all third-party labs, pathologists, and anesthesiologists in my network?”

- Review your deductible clause: Log into your portal today and check your exact out-of-network maximums.

- Sign carefully: Never sign a blank “financial responsibility” waiver at the front desk before knowing who will process your tests.

- Leverage state laws: Check how the federal No Surprises Act and your local state laws apply to emergency vs. non-emergency billing.

- Never pay the first invoice: If you face a massive balance bill, do not pay it immediately. Call your insurance provider and demand an official audit.

(Sources: KFF Health News & NPR “Bill of the Month” Investigation Series)